Articles & Webinars

Explore articles and easy‑to‑follow webinars designed to help you understand ABLEnow and make confident, informed decisions about your savings.

Featured

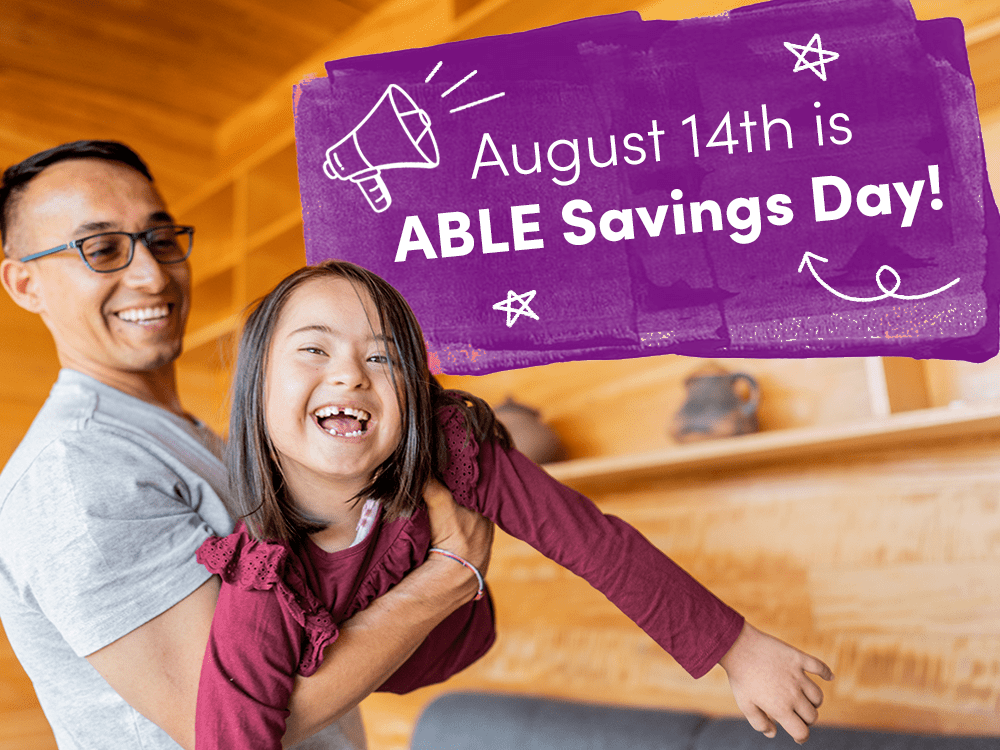

Article

Celebrate National ABLE Savings Day

Help educate more people about ABLE accounts.

Recent

Webinars

Get real answers to your questions about saving for higher education. View live or previously recorded webinars to learn more about Invest529 programs.

Upcoming Events

Aug

18

2026

Testimonials

Additional resources

Stay in touch

Sign up for the newsletter to get the latest information

* = required